Before You Sign: 10 Questions to Avoid Hidden Solar Fees

Preventative checklist of critical questions to ask before signing any solar contract to uncover hidden costs and avoid common financing traps.

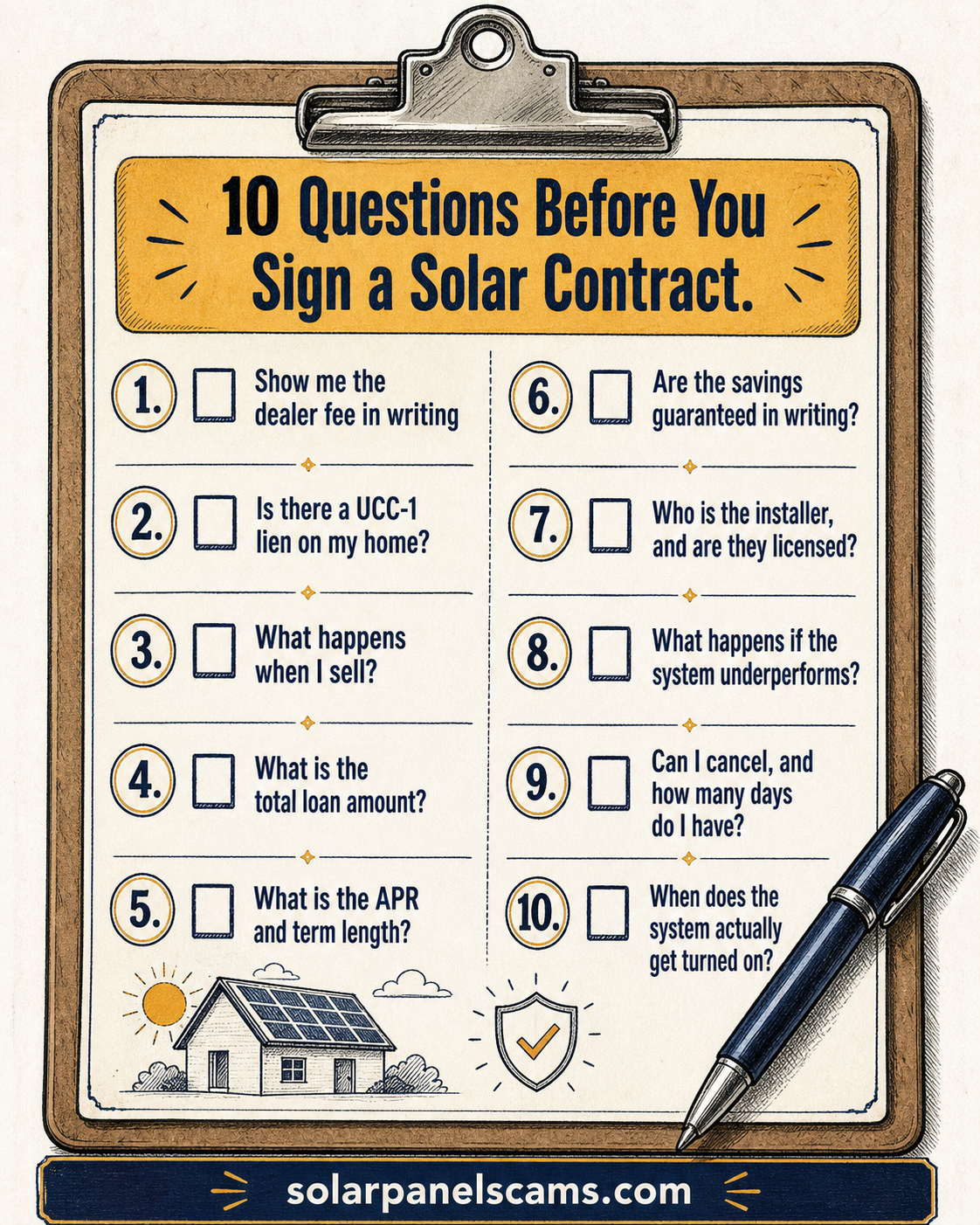

Before signing a solar contract, force the economics and legal obligations into writing. The most important questions are the cash price, financed amount, dealer fee, lien or UCC filing, cancellation deadline, payment trigger, tax-credit assumption, equipment ownership, warranty backer, and home-sale transfer terms.

Disclaimer: This article is for informational purposes only and does not constitute legal advice. Always review a solar contract with an attorney or financial advisor before signing.

Overview

The solar salesperson has an answer for everything: zero money down, instant savings, easy monthly payments. But what they often avoid telling you — the dealer fees that inflate your principal by 30%, the UCC-1 filing that clouds your title for 25 years, the PACE assessment that takes priority over your mortgage — is what turns a "great deal" into a financial disaster. The best defense is asking the right questions before you sign. Here are ten questions designed to surface what the sales pitch is designed to hide.

For deeper checks, pair this list with the solar dealer fees explainer and the door-to-door contract cancellation guide before you sign anything.

Treat the checklist above as a pre-signing script. Ask each question in writing, require the answer in the proposal or contract, and do not accept "we will explain later" as an answer. The most expensive solar problems usually appear in four places: the loan amount, the cancellation notice, the installer identity, and the title/lien language.

The 10 Questions

1. What is the dealer fee on this loan, stated as both a dollar amount and a percentage of the system cost?

Dealer fees — hidden origination costs that solar lenders charge installers for offering low APR loans — typically range from 25% to 31% of the system price. A $30,000 solar system can become a $40,000 loan principal overnight, with the difference buried in the "amount financed." Under California SB 784, solar salespersons must now disclose dealer fees. In other states, the burden remains on you to ask.

2. Will a UCC-1 financing statement be filed, and what collateral does it describe?

Get the exact collateral description in writing. If it says "all improvements and fixtures" or "all personal property," you are potentially encumbering far more than the solar panels. Demand language that limits the collateral to the specific equipment only.

3. Is this PACE financing? If so, what is the total assessment amount, the interest rate, and the lien priority?

PACE is not a loan — it is a property tax assessment that creates a first-priority lien ahead of your mortgage. Ask explicitly: "Is this PACE?" Salespeople sometimes use euphemisms like "property tax financing" or avoid the term entirely.

4. What is the total cost over the full term, including all escalators, fees, and taxes?

The monthly payment quoted today is not necessarily what you will pay in year 5 or year 15. Most solar PPAs and leases include annual escalators — often 2.9%. Ask for a payment schedule showing every year's obligation through the contract end.

5. What are my cancellation rights, and what happens if I cancel?

Under the FTC Cooling-Off Rule (16 CFR Part 429), door-to-door sales carry a 3-business-day right to cancel. If the contract was signed at your home, ask for the cancellation form. If none is provided, your cancellation rights may extend beyond 3 days. The Truth in Lending Act (TILA) also provides rescission rights for certain consumer credit transactions.

6. Is the payment schedule tied to milestones — specifically, when does the first payment become due?

Some contractors demand payment in full before installation is complete or before the system passes inspection. Tying payments to milestones — deposit, installation start, inspection pass, permission to operate — protects you from paying for work not yet done.

7. Who claims the federal tax credit, and what happens if I am not eligible?

The 30% federal solar tax credit is not automatic — it requires sufficient tax liability. If the contract prices the system assuming you receive the credit, and you do not qualify, you could be left covering the shortfall. Confirm who claims the credit and what happens if eligibility changes.

8. What warranties cover the system, who backs them, and for how long?

Distinguish between manufacturer warranties (panels, inverters), installer workmanship warranties, and production guarantees. Ask whether the warranty is backed by the installer, a third-party insurer, or the manufacturer — and whether the installer will still be in business when a claim is needed.

9. Who owns the equipment, and what happens to it at contract end?

In a PPA or lease, the solar company owns the panels. At the end of the term — often 20 to 25 years — you may need to buy the system, extend the contract, or have the panels removed at your expense. Get the end-of-term options in writing before signing.

10. What happens if I sell my home?

Solar contracts survive the sale. Ask about transfer requirements, buyer credit qualifications, buyout costs, and prepayment options. A contract that cannot be transferred to an average buyer can render your home unsellable to FHA and VA borrowers.

Regulatory Backing

These questions are not hypothetical. California SB 784 mandates dealer fee disclosure. The FTC Cooling-Off Rule requires cancellation notice delivery. TILA requires clear disclosure of finance charges and APR. The Minnesota Attorney General's investigation into $35 million in hidden solar lender fees demonstrates that regulators are scrutinizing the very practices these questions target. Asking these ten questions — in writing, with answers retained — protects you at every stage of the transaction.

Official Sources Behind the Questions

- The CFPB's solar financing issue spotlight explains dealer fees, loan structures, and consumer risks in residential solar financing: CFPB solar financing issue spotlight.

- The FTC Cooling-Off Rule text explains cancellation requirements for covered home-solicitation sales: FTC Cooling-Off Rule text.

- The Department of Energy explains how leases, PPAs, loans, and cash purchases differ: DOE homeowner's guide to solar financing.

- The Department of Energy recommends verifying installer credentials, insurance, subcontractors, and certifications before hiring: DOE guide to choosing a solar installer.

- The Treasury advisory highlights solar complaints involving costs, savings, loans, tax credits, and aggressive sales tactics: Treasury consumer advisory on solar energy scams.

FAQ

Do I really need to ask all ten questions?

Yes — and get the answers in writing. Verbal assurances during a sales pitch are not binding. If the salesperson cannot or will not answer a question clearly, that is itself a red flag.

What should I do if the salesperson refuses to disclose the dealer fee?

Walk away. A refusal to disclose the dealer fee — which inflates your principal and increases the total cost of borrowing — is a strong indicator that other terms are being hidden as well. In California, such refusal may also violate SB 784.

Can I ask these questions after signing?

You can, but your leverage is significantly reduced once the contract is signed. The FTC Cooling-Off Rule gives you only 3 business days to cancel after signing. Asking before you sign is always the strongest position.

What regulatory bodies enforce these disclosures?

The CFPB enforces TILA. The FTC enforces the Cooling-Off Rule. State attorneys general enforce consumer protection statutes and — in some states — specific solar disclosure laws like California SB 784.

Got blindsided by a solar deal that did not deliver?

You may have a claim — and the law may make the company that defrauded you pay your legal fees. Our 2-minute eligibility check screens for the consumer-protection statutes that apply to your situation (TILA § 130, the FTC Holder Rule, your state UDAP) and connects you with a consumer-protection attorney in our network if you qualify. Use the eligibility form to route your facts through the right intake path.

Next Research Steps

Use these resources to connect this issue with the broader solar scam pattern, the relevant legal framework, and the next practical action.

Solar panel scams

Start with the main solar panel scams guide for the broad definition and recovery roadmap.

Solar financing fraud compensation

Use this guide for loan, dealer-fee, payment-jump, PACE, lease, and lender-defense issues.

Homeowner legal rights

Review cancellation, rescission, UDAP, TILA, Holder Rule, arbitration, and lawsuit options.